Welcome to our Financial Wellbeing Centre

At HEY Credit Union we know how important it is for both your physical and mental wellbeing to have your finances under control.

Our experienced staff team have put together some articles, handy tools and tips to help you to find out more about everyday money matters and feel more confident around your finances.

We hope you will find this useful – please let us know if there’s any other topics you would like us to cover.

Remember, the contents are for general information only and do not constitute financial, legal or any other form of advice.

Making a budget is the first step towards good money management. Here are some useful budget planners to help get you started:

Money Helper

Money Saving Expert

If you would prefer to plan your budget on paper, take a look at our very own printable Budget Planner.

Are you claiming the benefits that you are entitled to? Here are some calculators that you can use to find out:

GOV.UK

Are you paying the correct income tax? Check here:

Money Saving Expert

Listen To Taxman

Want to build your financial knowledge? Here, we will be sharing information on topics which you may find useful both now and in the future.

Pensions - what are they and why are they important?

Financial Services Compensation Scheme (FSCS) - how your money is protected

Tax and National Insurance - what are they?

Recession - what does it mean?

Individual Voluntary Arrangements (IVA's) - be sure to know the facts before proceeding

Loan Agreements - what are their purpose?

Save up safely for Christmas - why you should be careful when choosing a savings club.

Credit Union vs bank - why choose one over the other?

Annual Percentage Rate (APR) - what is it?

Credit Reference Agencies - what are they?

Standing orders & Direct Debits - what are the differences?

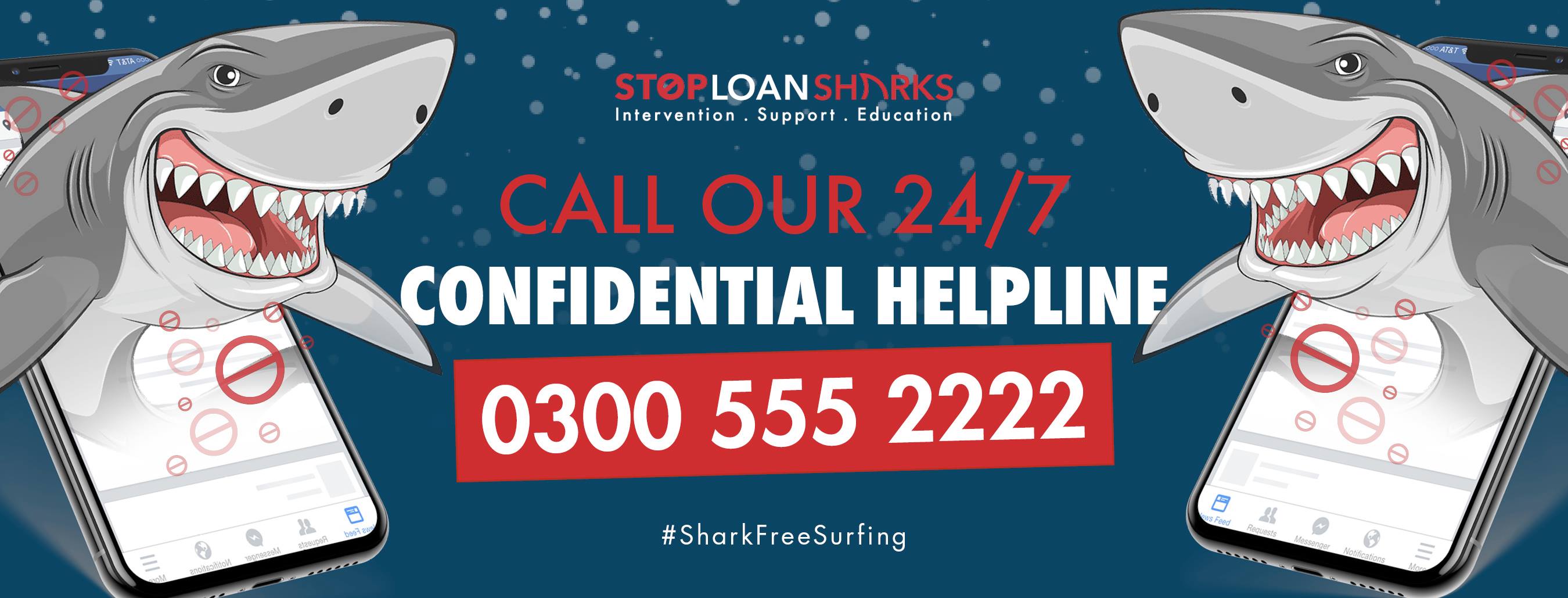

Loan sharks - who are they?

Educating children about money

Protecting yourself from scams and identity theft

What to do if you can't afford to make your Credit Union repayments

During these challenging times, we understand that our members may be facing financial uncertainty and we are here to offer a helping hand.

If you find your circumstances have changed, and are struggling to make payments, please contact our Member Solutions Team as soon as you can at membersolutions@hullandeycu.co.uk or on 01482 778753 (option 3)

We assess all circumstances individually and will discuss the right, responsible solution for you.

You can report a loan shark confidentially 24/7 on 0300 555 222, start a live chat, or email.

HM Treasury Factsheet - Autumn 2022

HEYCU - Cost of Living Extra Help - Feb 2023

East Riding of Yorkshire Council - Help for Households / Help for Businesses

Life isn’t always as easy and smooth sailing as we’d like it to be. If you’re in a situation where you don’t know where else to turn, there are many free and impartial organisations out there that can offer you support or advice:

It can seem overwhelming dealing with the death of someone close to you. There are a number of sources of support including your GP, community or faith groups, and organisations that you can turn to for help coping with grief:

Cruse Bereavement Care (and Cruse Bereavement Care Scotland).

Account

This is provided by a bank, building society or credit union which holds money for you. A current account is an everyday account which allows money to be paid in or taken out. A basic bank account is a special sort of current account which doesn’t usually allow you to overdraw. A deposit account is for your savings.

Annual General Meeting (AGM)

The yearly gathering of an organisation’s member-owners (in the case of a company – its shareholders). At an AGM, the directors present their annual report and the members can ask questions about performance, vote on important matters and choose the directors to be elected to the board.

APR – Annual Percentage Rate

This tells you the overall cost of borrowing, taking into account the interest you pay, any other charges, and when the payments fall due. You can use the APR to compare the cost of one loan with another. The higher the APR the higher the cost of the loan.

Arrears

Money owed that has not been paid by the date it is due.

Assets

Things that are owned such as cars, property, savings and money.

ATM

Stands for ‘automated teller machine’ and is another name for a cash machine.

Balance

The amount of money you have in your account at any particular time or which you owe on your credit or store card. It will be shown on your statement.

BACS

Bankers Automated Clearing Services – BACS is the usual way to transfer money from one bank account to another in the UK.

Balance Sheet

A financial statement that shows the organisation’s assets, liabilities, and member-owners’ funds (capital and reserves). It provides a snapshot of what it owns and owes on a particular date and helps anyone interested to judge how healthy it is.

Bank of England

The central bank of the United Kingdom. Its mission is to maintain monetary and financial stability and take action when needed, for example by changing interest rates. It also issues bank notes and regulates other banks and financial firms like credit unions, so that people know they are safe and sound.

Bankruptcy

A procedure where someone who can’t repay money they owe has their financial affairs taken over by an official who arranges to pay off as much as possible by selling the bankrupt’s assets. It usually lasts for a year but is likely to affect your ability to get credit for a further six years.

Beneficiary

The person or persons nominated (named) to receive a benefit of an insurance policy or funds in a credit union account upon the death of the account holder.

Borrower

A person or organisation that takes out a loan from a lender under an agreement to pay it back over a period of time, typically with interest.

Bounced Cheque

When a cheque cannot be paid because there isn’t enough money in the customer’s account.

Broker

Someone who buys or sells things on behalf of a person, such as stocks and shares or insurance, or undertakes to find them a loan. Commission is payable for the broker’s services.

Budget

A personal money plan which helps an individual to manage their income and expenditure. It usually covers a period of a month or a year, but can be for longer. Businesses and governments also use budgets.

CCJ

This stands for County Court Judgment. It is an order made by a judge for an outstanding debt which can affect your credit rating.

Capital

An amount of money that a person originally invests.

Cashback

A method by which you can draw cash from your bank account at supermarket checkouts when you pay for goods with your debit card.

Commission

Payment made to a salesperson or adviser by the provider whose products have been sold. It is generally based on the value of the sale and you pay the commission indirectly through charges built in to the product.

Credit

If your account is in credit, it means that you have money available to spend. If you obtain goods or services on credit, it means that someone, for example, a bank or credit institution, has given you the money to buy something. You must pay the money back, usually with interest.

Credit Card

A plastic card issued by a bank or building society which allows you to buy things and pay for them later. Your credit card issuer gives you a limit that you can spend up to on that account. You must pay back at least a minimum amount each month and usually interest will be charged if you do not pay off the full amount borrowed.

Credit Limit

The maximum amount allowed to be used on a credit card.

Creditor

A person or business that money is owed to.

Credit Rating

A credit rating is a measurement of a person’s ability to repay a financial obligation based on their income and past repayment history. It is often expressed as a credit score and is used by banks and other lenders as one of the factors to decide whether to lend money.

Credit Reference Agency

Credit reference agencies are firms which are allowed to collect and keep information about consumers' borrowing and financial behaviour. When you apply for credit or a loan, you sign an application form, which gives the lender permission to check the information they hold. There are three main credit reference agencies in the UK – Experian, Equifax and TransUnion.

Credit Report

This reveals whether you pay your bills on time, how much debt you have, how many times you've applied for credit, whether you've missed any payments, and if you've had any county court judgments (CCJs) filed against you. You can obtain one free of charge from a credit reference agency.

Credit Search

If you apply for credit (a loan) it is highly likely that the lender will carry out a credit search on you. This will help them to decide whether to offer you a loan or not. A credit search tells a lender how much credit you already have and how consistent you have been in making repayments and helps them to understand your financial behaviour.

Credit Union

Credit Unions were created to help members to save and have access to affordable loans from the savings the members have pooled together. They offer an ethical way to save and borrow on the basis of ‘people helping people’. Credit unions operate not-for-profit, as any surplus income made from the loan book is then shared among all the members by way of an annual dividend. All savings are 100% guaranteed by the Financial Services Compensation Scheme.

Current Account

A bank account which allows a customer to deposit money and withdraw money, by cash, cheque, standing order or direct debit.

Debit

Money owed to another person or business. A person who owes money to others is known as a debtor.

Debit Card

A plastic card used to pay for things in a shop, online, or to get cash from an ATM. The amount you pay or withdraw is taken directly from the bank account to which the card is linked.

Default

Failure to meet the financial obligations as agreed. People who do not make payments on a loan have ‘defaulted’ on that agreement.

Deposit

A sum of money which is placed in a bank, building society or credit union. Or, it could refer to the first instalment of a large purchase, for example a deposit on a house.

Dividend

The equitable division of surplus earnings to an organisation’s member-owners or shareholders.

Direct Debit

An instruction to your bank to release money automatically from your bank account to pay a regular bill. This is useful for frequent bills which are for different amounts each time, for example, telephone bills. You arrange this with your supplier and give them your bank details.

Debt Management Plan (DMP)

A DMP is an informal agreement between a debtor and a creditor whereby they come to an agreement in relation to repaying outstanding debt. You usually repay an amount every month which is then divided between all your creditors (companies who you own money to). Some creditors may freeze or reduce the interest rates, the DMP will continue until all the debts are paid back in full.

Doorstep Lender

Sometimes called Home Credit (or Home collected credit), this is where you borrow money and the lender calls at your home to collect the repayments. The loans are usually for small amounts are best avoided if you have other options as the high interest charges make it a very expensive way to borrow.

Faster Payments Service

A bank system that allows transactions by phone, internet and standing order to be made within two hours. This is the method HEY Credit Union usually uses to make payments to our members.

Fees

Payments made to a firm or person in return for services, for example bank charges or legal advice.

Financial Advisor / Independent Financial Advisor (IFA)

An adviser or firm that provides independent advice and is able to consider and recommend all types of retail investment products that could meet the needs and objectives of the person wishing to invest. IFAs are regulated by the Financial Conduct Authority. People often consult them about retirement planning, insurance protection, mortgages, tax and legal matters as well as investments.

Financial Conduct Authority (FCA)

The FCA is a financial regulatory body in the United Kingdom, which operates independently of the UK Government. Its role is to monitor the conduct of financial services firms to make sure they are treating customers fairly. It is financed by charging fees to the firms it regulates.

Financial Ombudsman Service (FOS)

The Financial Ombudsman Service (FOS) is a free and easy-to-use service that settles complaints between consumers and businesses that provide financial services.

Financial Services Compensation Scheme (FSCS)

The FSCS protects you when financial firms fail. If the firm you have savings with goes out of business, the FSCS steps in to pay you back your savings up to a maximum of £120,000.

Fixed Interest Rate

This is a rate that stays the same for a defined period during a loan.

Grant

A sum of money given to a person or organisation to fulfil a particular objective, for example research, business development or training. Grants are essentially gifts that do not have to be repaid if used appropriately.

Gross Income

The full amount of money earned before any deductions such as tax.

Health Cash Plan

An insurance-type product which pays out cash sums for particular health costs, such as if you have to go into hospital, need dental treatment, become pregnant or visit a chiropractor.

Hire Purchase Agreement (HP)

A form of credit agreement which allows you to pay for goods in instalments. Cars are often bought this way. You will not own the car until all the instalments have been paid. If you don’t make the payments as agreed, the car might be taken away from you (repossessed) and sold. You can’t sell the car without the permission of the lender until you have paid for it.

HMRC

Her Majesty's Revenue and Customs is a non-ministerial Government department responsible for the collection of taxes, administration of child benefits, the national minimum wage and issuing national insurance numbers.

Income Tax

A tax on personal income. Usually deducted directly from your wages or salary.

Inflation

The upward movement of prices (or earnings) over a period of time, which means the buying power of your money falls. A common measure of price inflation is the Retail Prices Index.

Interest

This is the reward you get for keeping your money in, for example, a bank or building society. Rates vary so you should shop around for the best deals. It is also the cost you pay when you borrow money through a loan or credit agreement.

Interest Rate

This is the percentage that is paid on savings or loans. A savings account that was offering 4% would give you a better return than one which was offering 2%. Similarly, borrowing money at 29% is going to cost you more than borrowing at 18%.

Individual Voluntary Arrangement (IVA)

A formal and legally binding agreement with your creditors to pay back your debts over a period of time. This means it’s approved by the court and your creditors have to stick to it. An IVA can be flexible to suit your needs but it can also be expensive and there are risks to consider as it is likely to affect your ability to get credit for a further six years.

Individual Savings Account (ISA)

A government scheme to encourage savings by offering tax incentives. ISAs can be used to make a wide range of investments through two components: cash (bank, building society and National Savings), and stocks and shares (unit trusts, shares, bonds and gilts).

Insolvency

A state of financial distress in which a business or person is unable to pay their bills. It can lead to insolvency proceedings, in which legal action is taken, and assets may be liquidated to pay off outstanding debts.

Instant or easy-access accounts

Savings accounts where you can withdraw your money without giving any notice or losing any interest.

Lasting power of attorney

A legal arrangement where you appoint someone to manage your financial affairs (and possibly health and welfare needs) should you lose your mental capacity.

Lender

An organisation or person that lends money.

Loan

An agreement between a lender and a borrower. The borrower agrees to repay the money borrowed over a period of time – normally with interest.

Loan Shark (or Illegal Lender)

An unlicensed moneylender who often targets families on low incomes or those in difficult times. Licensed moneylenders are regulated by the FCA. You can search the Financial Services Register to see if a lender is authorised to lend money and report illegal lenders anonymously: reportaloanshark@stoploansharks.gov.uk Telephone: 0300 555 2222 or text 07860 022 116

Minimum Repayment

The smallest amount you can pay towards money you owe on a credit card. It is stated on your monthly statement.

Money Laundering

Money laundering is the illegal process of generating money by criminal activity, such as drug trafficking or terrorist funding, and making it appear to have come from a legitimate source. Reports about suspected money laundering have to be sent to the National Crime Agency.

Net Income

The amount of income after all deductions (for example, tax and National Insurance). Also called ‘take-home pay’.

Notice accounts

Savings accounts where you can only withdraw money after telling the provider in advance. Some accounts waive the notice period, but you then lose interest instead.

Online Banking

A service which allows you to operate a bank account over the internet.

Overdraft – Arranged

An agreement with your bank which allows you to spend more money from your account than you have in it. You may be charged interest and fees to use this facility.

Overdrawn – Unarranged

If more money is withdrawn from your account than you have in it, you will be overdrawn. If you go overdrawn without asking the bank in advance, they might refuse to pay your cheques and charge you fees and a high interest rate on the money that you owe them.

Payday Loan

A relatively small amount of money lent at a high rate of interest on the agreement that it will be repaid when the borrower receives their next wages. Payday loans are best avoided because the very high-interest rates and fees often cause borrowers to get stuck in an ongoing cycle of problem debt.

Personal Identification Number (PIN)

A secret number, which you use with your bank card, to make withdrawals at ATMs. You must type this in to use the card. This ensures that no one else can use your card. You must always keep this number safe and not disclose it to anyone.

Prudential Regulation Authority (PRA)

The Prudential Regulation Authority (PRA), as part of the Bank of England, is the United Kingdom's prudential regulator for deposit-takers (banks, building societies and credit unions), insurance companies and designated investment firms.

Savings Account

A financial product to keep savings secure within a bank, building society or in a credit union. The amount you put in does not fall in value but may grow as interest is added.

Secured Loan

This is money borrowed from a lender, using your property or other asset as a guarantee of repayment. If the amount is not paid in full, the lender may take the property back (repossess it) and sell it.

Shares

Shares represent a slice of the ownership of a company and may give the right to vote on decisions about its running, also a share of the profits (dividends). In co-operatives such as credit unions, each member is considered to have one share, and therefore an equal vote with other members, and dividends are based on the use made of savings accounts and/or loans instead.

Standing Order

A method of paying regular amounts from your bank account automatically. You instruct your bank to pay the money for you to a particular person or company. It is your responsibility to change the payment if it needs to be altered.

Statement

A document from the bank, building society or phone provider, which shows all your recent payments into, and withdrawals from, your account. You should check it against your own records and contact the provider immediately if anything looks wrong.

Store Card

A plastic card issued by a shop that lets you buy goods at that store on credit. You must either pay the full amount, or something back each month.

Term

The time period over which you borrow or invest.

Unsecured Loan

This is money borrowed from, for example, a bank, which is not secured against your home. The lender may take court action against you for payment if you don’t pay the money back as agreed.

Utilities

Services such as gas, electricity and phone.

Withdrawal

What you are doing when you take money out of your account.

Treating Customers Fairly Champion - Awarded by Smart Money People at the Consumer Credit Awards 2025

Best Member Satisfaction Rating 2025 - Awarded by 1872° Culture in partnership with ABCUL

Protected by the Financial Services Compensation Scheme

Supporting the armed forces and veterans community

Proud Living Wage Employers

.png)